This post is for educational purposes only. PlanSmartFi is not a financial advisor. Always do your own research and consider speaking with a licensed financial professional before making any financial decisions.

The 50/30/20 Rule Canada: Does It Actually Work for Canadians?

Does the 50/30/20 rule Canada-style actually work? The rule is one of the most widely shared budgeting frameworks online. It is simple, memorable, and easy to explain. But for many Canadians, especially those living in Toronto, Vancouver, or other high cost-of-living cities, following it to the letter can feel impossible.

This post explains how the rule works, where it falls short in a Canadian context, and how you might adapt it to actually fit your life.

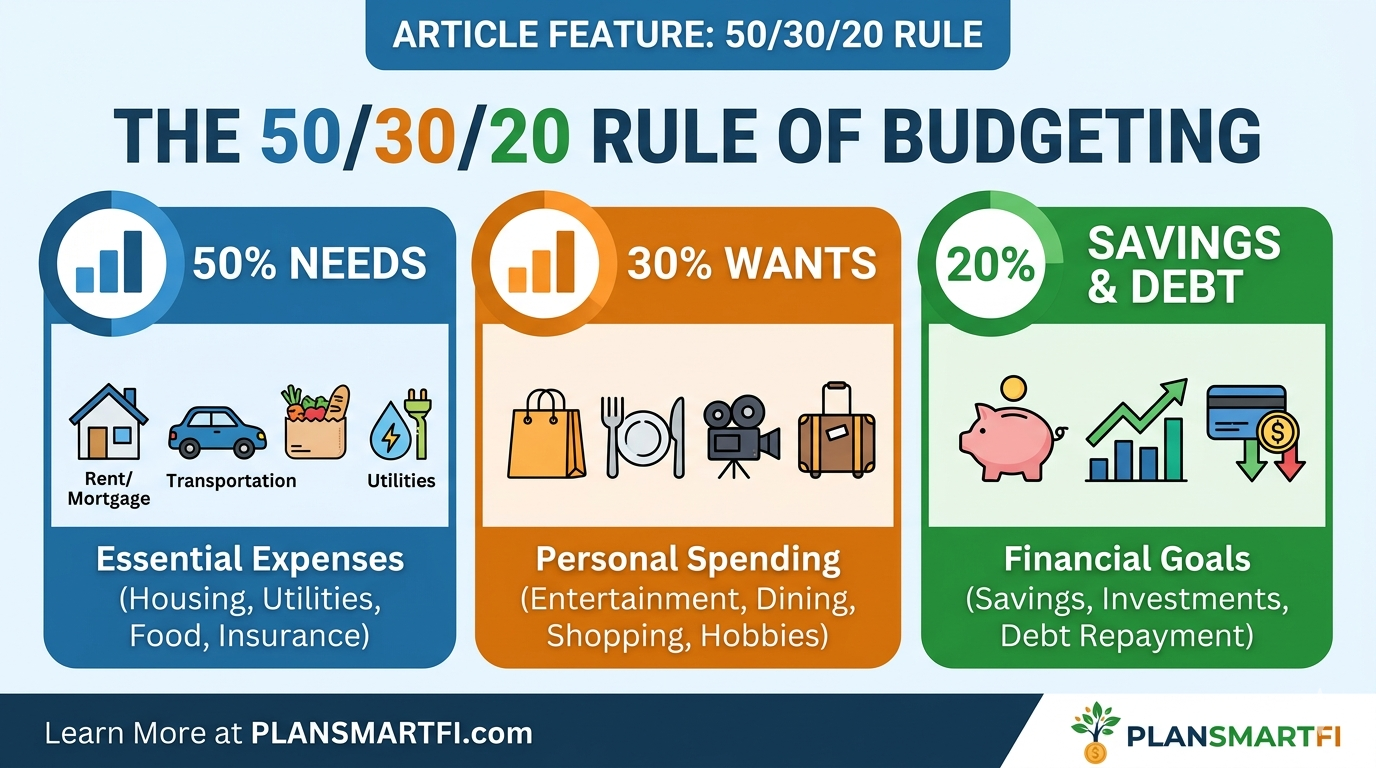

What Is the 50/30/20 Rule?

The 50/30/20 rule is a budgeting guideline that divides your after-tax income into three categories:

| Category | Percentage | What it covers |

|---|---|---|

| Needs | 50% | Rent or mortgage, groceries, utilities, transportation, insurance, minimum debt payments |

| Wants | 30% | Dining out, subscriptions, travel, entertainment, shopping |

| Savings and debt repayment | 20% | Emergency fund, TFSA, RRSP, FHSA, extra debt payments |

The rule is based on after-tax income, meaning what actually lands in your bank account after income tax, CPP contributions, and EI premiums are deducted. It was popularized by U.S. Senator Elizabeth Warren in her book All Your Worth, though the concept has been adapted widely since.

The appeal is its simplicity. You do not need a spreadsheet or a detailed line-by-line budget. You just need to know roughly where your money is going.

Where It Works Well

For someone earning a moderate income in a mid-size Canadian city, the 50/30/20 rule can be a reasonable starting point. It works best when:

- Your housing costs are well under 30% of your take-home pay

- You are not carrying high-interest debt that demands aggressive repayment

- You want a simple framework without the complexity of a detailed budget

- You are just starting to think about budgeting and need somewhere to begin

As a rough check rather than a strict prescription, many people find it useful. If your needs are eating 70% of your income, the rule immediately tells you something is out of balance, even if it does not tell you exactly how to fix it.

Where It Falls Short in Canada

The 50/30/20 rule was designed with American incomes and housing costs in mind. In a Canadian context, several factors can make the 50% needs category very difficult to hit.

Housing costs in Toronto and Vancouver

In many Canadian cities, rent alone can consume 40% to 50% of a moderate after-tax income, before you factor in groceries, transit, or insurance. The Canada Mortgage and Housing Corporation (CMHC) considers housing affordable when it costs no more than 30% of before-tax household income. For a large portion of renters in Toronto and Vancouver, that threshold was crossed long ago.

Example: Toronto renter, $60,000 gross income

Approximate after-tax take-home: ~$47,000/year (~$3,917/month)

50% needs budget: ~$1,958/month

Average one-bedroom rent in Toronto was around $2,400/month as of 2024, though this varies by neighbourhood and can change over time.

Rent alone can exceed the entire needs budget before any other essential is added.

This is not a personal finance failure. It is a structural reality that a generic budgeting rule cannot account for.

Canadian tax rates

Canada’s combined federal and provincial income tax rates, along with CPP and EI deductions, mean after-tax income is often meaningfully lower than gross income. The 50/30/20 rule applies to after-tax income, which is correct, but Canadians need to be clear on what their actual take-home pay is before running the numbers.

Debt loads

Student loans, car payments, and lines of credit are common for many younger Canadians. Minimum debt payments fall under needs, which can push that category well above 50% on their own, leaving little room for groceries or utilities.

A Modified Approach That May Work Better

Rather than abandoning the rule entirely, many people find it more useful to treat the percentages as a starting point and adjust from there based on their actual situation. Some common modifications include:

| Situation | Possible adjustment |

|---|---|

| High rent in Toronto or Vancouver | Move to 60/20/20 or even 65/15/20, and focus on keeping savings at 20% |

| Carrying high-interest debt | Temporarily shift to 50/20/30, directing extra toward debt repayment |

| Low income or entry-level salary | Prioritize needs and a small savings habit; reduce wants aggressively until income grows |

| Dual income household | Run the calculation on combined after-tax income for a more accurate picture |

The underlying principle worth keeping regardless of the split: pay yourself first. Even a small, consistent contribution to savings or debt repayment matters more than hitting an exact percentage.

One clarification worth making: not all needs carry equal weight. Groceries, utilities, basic insurance, and housing are core needs that should be protected first. If your needs category is running over budget, the first place to look for reductions is expenses like cable packages, premium phone plans, or subscriptions that have crept into the needs column but could reasonably be trimmed or moved to wants.

How to Apply It in Canada: A Simple Starting Point

If you want to try the framework, here is a practical way to get started:

If you want a ready-made tool to help with this, the PlanSmartFi free budget template is a good place to start. It is designed for Canadians and lets you map your income and expenses without building a spreadsheet from scratch.

- Start with your actual after-tax income. This is what hits your bank account each month, after income tax, CPP, and EI are deducted. If your income varies, use a conservative average.

- List your fixed needs. Rent or mortgage, minimum debt payments, insurance, phone, and transit. Add them up and see what percentage of your take-home they represent.

- Assess the gap. If your needs already exceed 50%, that is useful information. It tells you the standard rule does not fit your situation and you need a modified split.

- Protect the savings percentage first. Whatever split you land on, many people find it helpful to treat savings as a non-negotiable line item rather than whatever is left at the end of the month.

- Revisit every few months. Income changes, rent increases, and new expenses mean your split will shift over time.

Quick check: are your needs above 50%?

Take your total fixed monthly expenses (rent, debt payments, insurance, utilities, groceries, transit).

Divide by your monthly after-tax income.

If the result is above 0.50, the standard 50/30/20 split needs adjusting for your situation.

Where the 20% Goes in a Canadian Context

The savings and debt repayment bucket is where Canadian-specific accounts come into play. The 20% category could include contributions to:

- TFSA for flexible, tax-free savings or investing

- RRSP for retirement savings with a tax deduction today

- FHSA if you are saving toward a first home purchase

- Emergency fund if you are still building one

- Extra debt payments above the minimum, particularly on high-interest debt

Most Canadians are not doing all of these at once. Prioritizing which bucket gets funded first depends on your situation. If you are still building an emergency fund, that is a reasonable first focus before directing money into investment accounts. Our post on how to build an emergency fund in Canada from scratch covers that step in detail.

Frequently Asked Questions About the 50/30/20 Rule

Is the 50/30/20 rule based on gross or after-tax income?

After-tax income. You should use what actually lands in your bank account each month, after income tax, CPP contributions, and EI premiums are deducted. Using gross income will make your budgets look larger than they actually are.

Does the 50/30/20 rule work for low-income Canadians?

It can be difficult to apply when income is limited, because fixed needs like rent often consume a much higher percentage of take-home pay. In that situation, many people find it more practical to focus on covering essentials, building even a small savings habit, and reducing the wants category significantly until income grows or fixed costs decrease.

Where do debt payments go in the 50/30/20 rule?

Minimum debt payments are generally considered a need and belong in the 50% category. Extra payments above the minimum, where you are actively trying to pay down debt faster, are often placed in the 20% savings and debt repayment category.

What counts as a need versus a want?

Needs are expenses you cannot reasonably live without: housing, basic groceries, utilities, essential transportation, insurance, and minimum debt payments. Wants are things that improve your quality of life but are not strictly essential: dining out, streaming services, travel, and discretionary shopping. Some expenses sit in a grey area, like a phone plan, which many people consider essential today but the tier of plan chosen may be a want.

The Bottom Line

The 50/30/20 rule Canada adaptation is a useful starting point, but it is not a universal formula. For Canadians in high cost-of-living cities, or anyone dealing with significant debt or a lower income, the standard split will often not reflect reality. That does not mean the rule is useless. It means treating it as a framework to adapt rather than a target to hit exactly.

The most important number in the rule is arguably the 20%. Protecting a portion of your income for savings and debt repayment, whatever that percentage ends up being for your situation, is the habit that tends to matter most over time.

Financial Disclaimer: The information in this post is for educational purposes only and does not constitute financial advice. PlanSmartFi is not a financial advisor. Always do your own research and consider speaking with a licensed financial professional before making any financial decisions.